Let’s complain about the global trade | Luminor

Let’s complain about the global trade

Autumn 2019: Global economic outlook

Trade is the predominant risk for the year causing heightened financial and economic volatility. Global trade growth did fall markedly below the global GDP growth in Q1 with a meagre ca 0.5% y/y expansion reflecting broad-based deceleration and ongoing adjustment of global value chains. Furthermore, trade tensions have re-escalated since the summer months, dragging down economic confidence across the advanced and emerging markets space. However, the economic sentiment readings have been falling from exceptionally strong levels and remain still not far from historical average levels, which cannot be associated yet with real economic stress.

There is no doubt that prolonged global trade tensions and related geopolitical risk factors, along with the rising threat of protectionism and vulnerabilities in emerging markets, constitute headwinds for the advanced and emerging markets alike.

So it is not surprising that previously hefty growth is trending down towards the potential in a number of advanced countries. Export dependent countries related to global trade are more prone to experience protracted cyclical weakness with a risk of triggering a number of technical recessions1 including in Europe.

There are, however, a number of impending structural challenges ahead as well on the longer-term horizon. Namely, there is still a puzzle with overall slow productivity growth, aging and last not least possible higher levels of protectionism as a new normal. This will raise the need for countries to devise in time their growth-enhancing reforms with innovation and global competitiveness in focus.

The above mentioned headwinds have left the global manufacturing sector on a protracted soft patch and continue to depress the economic sentiment. Prolonged trade tensions among the major economic heavyweights — the U.S. and China, have reduced trade flows and appetite for investments globally.

Manufacturing confidence in particular has been affected the most both in advanced and emerging market alike with weakness expected to extend well into H2 and beyond. Trade negotiations between the U.S. and China are expected to continue after some summer setbacks, but there is a growing risk of new tariffs and trade retaliation from each side before reaching a doable compromise. This heightened uncertainty or known unknowns has global implications and is visible in financial markets and deteriorating fundamentals for the global economy.

For Europe, and UK in particular, there is a looming risk of no-deal Brexit, which besides unwanted economic uncertainty holds back some of the private sector investments. Also Italian economy faces a government reshuffle, which comes at a time when budget position is strained the most and growth is missing. In a number of highly indebted countries there is limited ammunition left (in fiscal space) should the new economic shocks hit.

Moreover, there are other geopolitical tensions and strains (involving notably Iran, Hong-Kong, India-Pakistan, Syria ex cetera), which can potentially exaggerate the already rather toxic mix of external risk factors cooling the economic recovery. Hence softer momentum for trade leaves the domestic demand for a time being as the key engine for growth in euro area including the open Baltic economies.

Slower growth environment in the world and euro-area economy has increased recession risks for the weaker performers. A number of small cracks have emerged in the world economy testing the risk appetite of markets following the recent sharp sell-off we saw in risk assets last fall. Namely, there is an increasing tendency for global flattening and inversion of yield curves (a typical sign of economic risks ahead) in global bond markets. However, what is comforting is the fact that credit markets have largely spelled the flight to quality with credit spreads remaining largely untouched in advanced countries.

The record low yields will remain a topic of controversy. Government bond rates are making new lows with U.S. treasury 30 year bonds dipping in mid-August below the 2% levels, which we have not seen for decades. Overall, low rates bode well for the domestic economies, with some support coming from construction and real-estate sectors in a number of European countries with close economic ties to the Baltic countries. When manufacturing is in doldrums, we need services and housing to strive.

Chart 1. Trade tensions weighs on global growth outlook

We share the view that yield curve inversion (between short and long-term rates) this time is no actual sign of recession knocking at the doorsteps yet, but rather a reflection of flight to quality and slightly overoptimistic market expectations of future policy easing in the context of overall benign inflation and growth environment. Most of the global institutions including IMF and central banks have indicated that baseline is not for the world economy stalling or recession. We don’t expect a recession in the euro area as a baseline in near term, but downside risks are intensifying subject to heightened trade uncertainty and escalation in trade protectionism involving advanced countries including the U.S. and Europe. The Baltic economies’ growth will comfortably exceed the average growth in the single currency area.

Global manufacturing remains in the epicentre of economic slowdown, while the consumer holds strong. The hallmark of the protracted weakness in the global economy seems to be still very much a broad-based slowdown in the manufacturing sector. Manufacturing has been subject to tariff disputes, adjustment of global value chains, and is the main victim of the global auto sales slipping from China to recently also in a number of European countries. European new car registrations were down in Jun -3.1% y/y. Car manufacturers have faced multifaceted headwinds including Chinese consumers cutting back on big-ticket goods, stricter emission standards and costly shift from diesel to electric. To the extreme end in Norway half of new car sales is electric vehicles.

The weaknesses in the industrial sector in Europe has been contained largely within the manufacturing space, with capital and intermediate goods production underperforming relative to consumer goods. Industrial production volumes in euro area were down -2.6% y/y in Jun. The overall economic environment is however not recessionary and the reasons are the following.

Services continue to outperform manufacturing. Namely, there is still limited spill-over to the stronger performing services sector, which benefits from domestic demand led growth. The consumer holds still strong in advanced countries and the labour markets actually continue to tighten further, albeit at a moderating speed.

For example, employment rate in euro area was up 0.2% q/q in Q2 (1.1% y/y) following 0.4% q/q (1.3% y/y) leap in the stronger first quarter. Also wage growth has picked up yielding euro-area consumers real yields in the order of 1 to 2% (with nominal wages up 2.4% y/y in Q1).

The Baltic countries, which have recovered faster from the global crisis, are experiencing currently vigilant real wage growth, which will continue to power consumption growth. Income convergence with the West and low unemployment will help to keep consumers resilient in the face of heightened uncertainty abroad. As the economic growth moderates so does the wage growth, but it will be gradual.

Also across the Atlantic, the recent figures from the U.S. economy continue to be encouraging with regard to consumer demand and confidence. Retail sales growth remained healthy both for the Jun and July month.

Moreover, unemployment rates have reached pre-crisis low level. There is no noticeable deterioration in the labour demand (evident in vacancy rates or hours worked).

Global trade is today clearly the number one complaint. However, the second single major factor, which companies of global reach complain about, is an increasing lack of qualified labour. In context of still healthy, albeit slowing overall growth, this does not signal that a noticeable turnaround in advanced countries labour markets to the softer tunes is around the corner beyond the manufacturing sector. The recent reporting season has indeed brought about an increasing number of earnings warnings. The main reason cited has been rightly so challenges with global trade.

There are risks that slower global demand will lead an increasing number of companies to revisit cost cutting in case orders remain weaker for longer. There is a squeeze on profit margins since companies have limited capacity to pass on the rising wage costs to the consumer given muted export prices. Remarkably, producer prices for the largest global manufacturer and exporter China have again turned into the deflationary trajectory since June. Chinese economy is experienced a slowdown including its industrial sector.

Furthermore, commodity prices (including oil, gas and metals) remain muted as global trade and demand slows. Notably, oil has fallen since touching annual high in late April. Worldwide demand for petroleum-derived fuels has been imperilled by a protracted trade negotiations between the U.S. and China.

Overall, the overall picture is of slower growth outlook in the key export markets of Baltic countries, but no hard recession looms on close horizon, so our baseline is softer growth ahead. There are clear risks from the escalation of trade tensions, which combined with above-referred geopolitical risks, can push some European countries into technical recessions. Companies operating in less cyclical sectors and in domestic markets are not sheltered, but do better relatively better on average in this benign global trade environment.

Key export markets for the Baltics continue on the growth path. Namely, euro area, the key destination of Baltic exports, is expected to benefit from tighter labour markets and support from domestic demand (including recovering investments). Growth will likely gather only slight momentum in the following years after subdued ca 1.2% y/y growth at most in the current year.

The rebound of activity outside the EU remains subject to lessening of global trade tensions, and with economies supported by easing of global financial conditions and policy stimulus in some emerging economies. The balance of risks remains tilted to the downside with risks of spillover of manufacturing weakness to other parts of the economy without sufficient further stimulus.

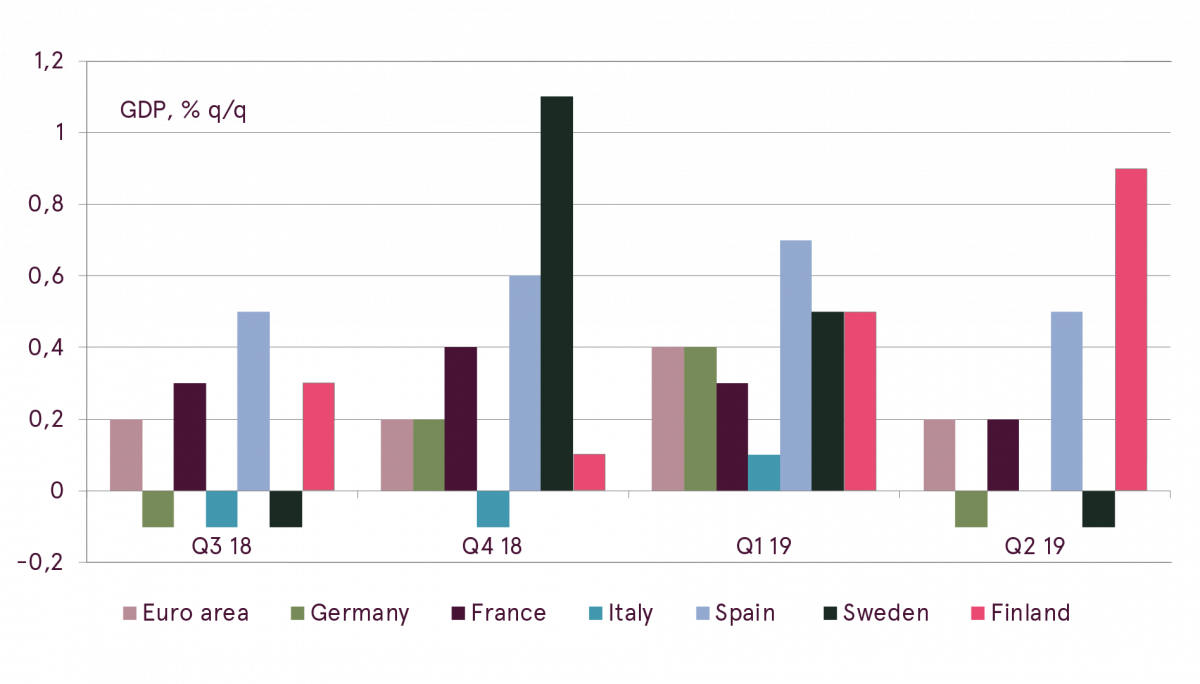

Chart 2. European growth momentum softer in Q2

Euro-area GDP decelerated noticably last fall to only 1.2% y/y (0.2% q/q) in Q4 2018 with softer contribution from industry and trade plus a drag from inventory adjustment. However, euro-area economies managed to resist a further moderation in momentum in the spring months with Q1 growth at 1.2% y/y (0.4% q/q), actually slightly exceeding expectations.

Summer months have unfortunately experienced a re-intensification of global trade tensions spanning beyond the majors, the U.S. and China, to reach also Japan and South-Korea. Global trade softness has weighted in particular on manufacturing heavy-weights. In particular, Germany, the largest export-dependent manufacturing hub among euro-area countries and a significant auto production base, has suffered relatively more from global trade moderation and uncertainty.

What is relevant is that among the largest euro-area countries, growth contracted in Q2 only in Germany, and by a small margin (-0.1% q/q), following a rather positive first quarter spurt. Italy did manage to just break-even (0.0% q/q), while France and Spain experienced only marginally softer advance. Overall, euro area expansion did expectedly continue, albeit at a softer tune with the annual growth holding still slightly above the one percent mark (1.1% y/y in Q2).

Also the open Nordic economies continue to face the heightened external uncertainty with the support from strong labor markets and healthy state of public finances. Monetary conditions are beset on the easing path with diminishing rate expectations accompanied by substantially weaker currencies in August. Even Norwegian central bank has signalled about pulling back from rate hikes not to ride against the tide of further monetary accommodation prepared by other global central banks.

Growth is now beset on a gradual moderation path in the norther region deeply integrated with Baltics. Among the Nordic countries, Norway is outstanding in terms of growth momentum benefiting from recovering oil investments, tight labour markets and favourable construction pipeline. Sweden economy open to global trade (and UK and Germany) did experience softness in Q2 (-0.1% q/q), while Finland manged to pull out a rabbit with a decent 0.9% q/q sprint resisting moderation calls. The overall trend is for slower growth over the next years, raising the discussions about growth enhancing reforms and possible fiscal stimulus. Export figures of

Baltic countries towards Nordic countries has remained overall positive. There are increased benefits from deep integration with the Nordic economies.

The Baltic states along with some CEEC peers like Slovakia constitute today one of the most dynamic economies of the EU. During the last three years Euro area including the Baltic countries have enjoyed a strong broad-based recovery reflected in above-trend growth and tightening labour markets. The average growth rate for 2017-18 has exceeded 4 percentage points in Estonia and Latvia, with a robust 3.8% y/y boost in Lithuania. This compares to a close to two percent average GDP advance in euro area.

With an employment-rich recovery in the Baltics, the labour participation rates (especially in Estonia) are making new record highs and unemployment rates have approached pre-crisis lows along with other faster evolving euro-area peers. However, growth is set to gradually moderate over the next two years, albeit from the high levels. Positive surprises cannot be excluded if global trade uncertainty wanes as economies benefit from stronger domestic demand including infrastructure projects (such as Rail Baltica). Gradual moderation leaves labour markets firm and tight, as European economies go through the current soft patch in the global trade.

A shift from de-synchronized growth to synchronized moderation of growth is expectedly proceeding as was our previous call with key risks for the open Baltic economies emanating from trade frictions hitting advanced countries. Global trade slowdown remains the root cause for the weakening growth outlook and emerging downside risks for the euro area including the Baltic economies. Trade remains likely the key concern and complaint for the industry.

Aging will affect the Baltics to the same degree as other euro-area peers

During the current good above-trend growth years the time is ripe for the Baltic economies to address some of the supply side reform agendas to enhance the long-term growth potential of the otherwise fast evolving economies. Growth constraints can arise from already tight labour markets, whereas the still low income levels compared to euro-area average do not help to compete for the best talent. The convergence of income levels to euro-area average levels has a long road ahead with the prosperity ultimately resting on future productivity gains.

Hence, it will be crucial for Baltic export-dependent economies to invest in new technology and machinery to achieve the benefits from early adopters and technology innovators. Economies will be devising their national reform agendas for 2035. Would be great if the future reforms will re-focus on long-term growth-enhancing reforms and productivity enablers, among which one can list education reform, innovation agenda and research and development. Smart infrastructure is one potential avenue to exploit further to better connect Baltic economies to digitalising global economies. It is increasingly the services segment (including business services, ICT, advanced engineering, e-commerce ect), which is the emerging driving force for the economies.

Baltic countries have over the last decade made considerable progress by driving unemployment rates down to close to pre-crisis lows. With Europe facing common aging challenges, there will be ample opportunities to further enhance the opportunities for the elderly by maximising their income from longer and more rewarding participation in the labour market. The income maximising opportunities calls for structural changes and politically less-rewarding structural reforms, which do not often yield immediate benefits.

Forthcoming gradual aging of societies is related to rising costs for health-care and social expenditure. European approach is aimed at the family of wealthy states, so there is no much room for low cost business. Consequently long-term strategies have to maximise quality employment opportunities. This requires constant drive for innovation, globalising smart ecosystem open to trade. Labour markets are open in the Baltics and with the rising income level and investment into novel technologies plus sustainable environment, companies will be better positioned to attract global talent and risk capital. ICT sector’s advance in the region has been a promising start to build upon.

One would wish also a smart savings system for retirement, with Estonia currently in the middle of undergoing rather notable changes to the pension system by shifting more responsibility for investment decisions to savers. It will be too early to count the apples after say two years, as such profound system changes would need to be tested over the economic cycle.

It is easy to complain today about the global trade and revert to comparatively easier fiscal demand stimulus options in case of spill over of weaknesses to services. However, most viable durable solutions for prosperity and faster long-term growth (at higher capacity utilization levels) rely increasingly upon enhanced focus on targeted structural reforms and investments.

Making banking delightfully easy