Coronavirus – new “Black Swan” or buying opportunity? | Luminor

Coronavirus – new “Black Swan” or buying opportunity?

Darius Svidleras

Investment Portfolio Manager

- Rapid spread of novel Coronavirus in China may shut down 2nd largest global economy from the rest of the world for weeks, if not months, potentially leading to another round of global economic slowdown

- Actions of central banks may prevent significant sell-off in equity markets, and if situation with virus stabilizes, strong rally may follow

- The recent correction has helped reduce excessive optimism in the market and investor sentiment is no more a headwind for the global equities

Black Swan – is the name given to extremely rare unforeseen events, leading to severe negative consequences. Examples of such events include September 11, 2001 terrorist attacks, 2008 collapse of Lehman Brothers, 2011 Japanese earthquake and Fukushima nuclear accident and some other observations. With the onset of new decade, we are potentially witnessing another black swan in the making – novel coronavirus (2019-nCoV1) from China.

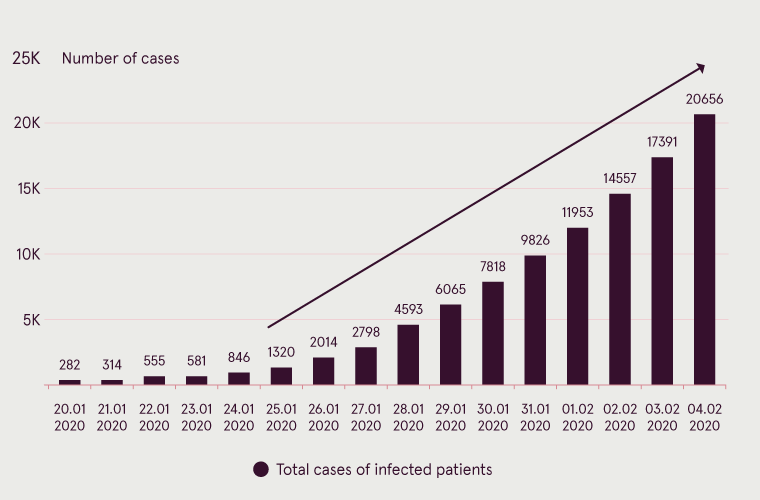

There are several reasons why situation with the new virus is so serious. First of all, so far virus is spreading almost exponentially. If there were only 282 confirmed cases of infected patients on 20th January, after about two weeks there were already more than 20000 registered cases of disease. Secondly, so far there is no vaccine against the virus, and death rate remains high, especially if measured as a proportion to recovered patients. Thirdly, it may take up to 14 days for the first symptoms of virus to emerge in patients, thus there may be significant delay in how fast the illness is detected. In addition, due to shortages of medical infrastructure in China, potentially not all cases of disease are being reported by the population. Finally, apart from China, first cases of coronavirus were already registered in 27 other countries, including USA, Germany and Australia. As a result, World Health Organization had to announce global health emergency on 30th January 2020.

Number of coronavirus cases by date

Source: WHO

Therefore, in order to contain spread of coronavirus further, as situation is becoming exceedingly dangerous, rather significant measures are being taken in China and worldwide. Chinese officials have already closed on quarantine more than 15 cities with more than 50 million of population. According to CNBC, in at least 24 provinces that account for around 80% of Chinese GDP businesses will not be resuming work until at least 10th of February. In addition, heavy restrictions are put on travel inside the country, while many global airlines cancel flights to and out of China. Global companies are also temporarily closing their operations inside the country, for example, Apple has closed all its stores in the country until at least 9th of February.

Thus, with cautionary measures being taken there are good odds that spread of disease would be limited only to certain areas inside China. However, for global economy and financial markets, even such outcome possesses major risks. China is responsible for around third of global economic growth and its GDP constitutes 16% of the global GDP, making it second largest economy after USA. In addition, China consumes more than half of global industrial metals, including copper, steel, aluminum and iron ore, and around one third of global vehicles and smartphones. Majority of global corporations has one or the other link to China – with country being either one of the largest markets for sales, or one of the largest places were production facilities are located. If we again take Apple as an example, majority of iPhones are being assembled at their factories in China. And if these factories would need to be closed due to threat of virus, negative impact on the financial performance of the company may turn out to be quite significant.

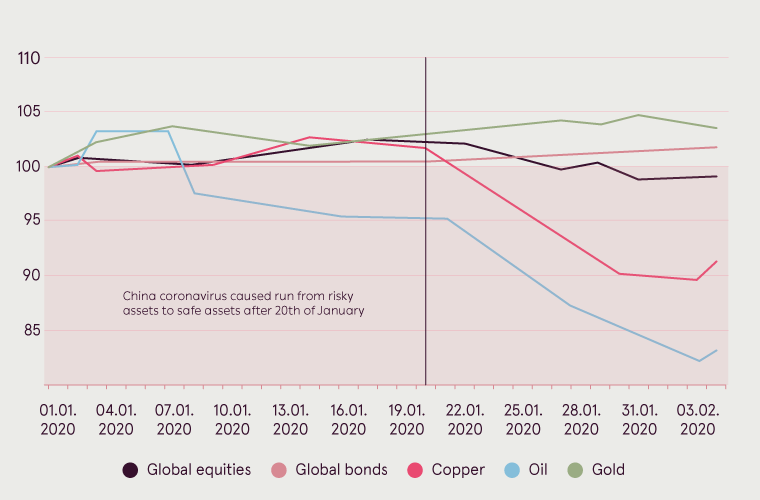

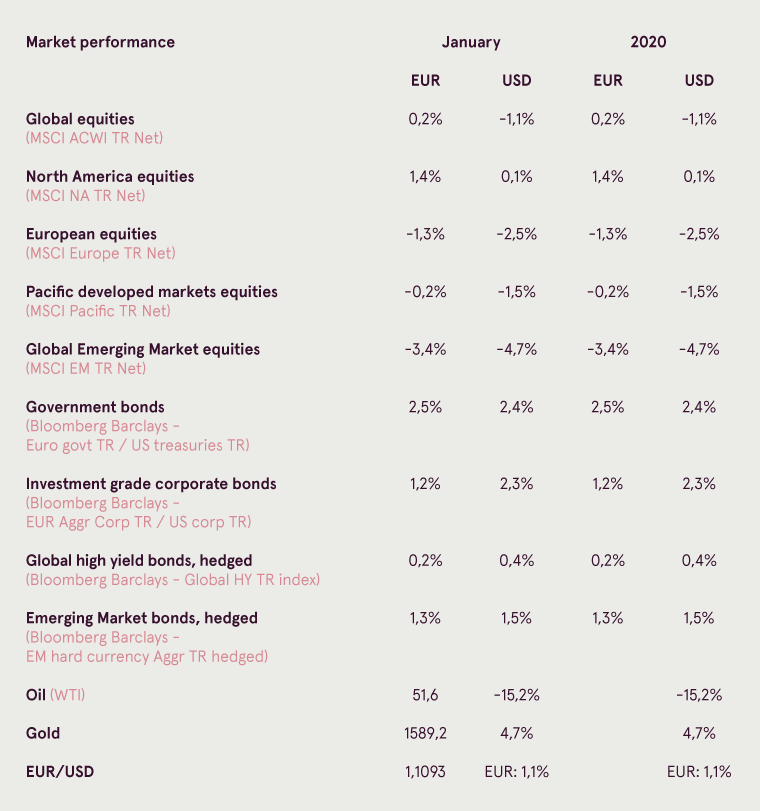

Performance of selected assets since 1st January 2020

Source: Bloomberg

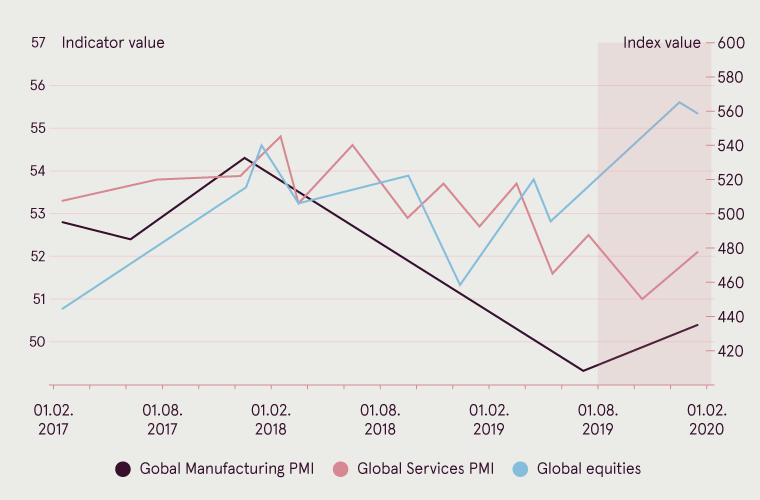

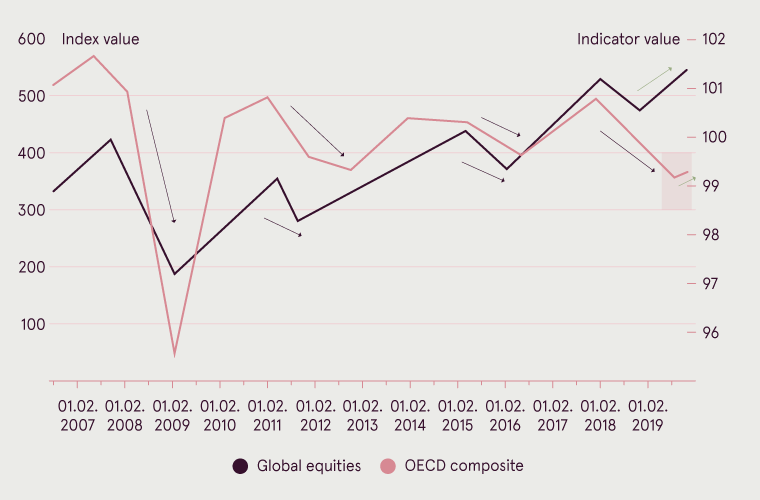

It is clear already now that recent events should slow down both Chinese and global GDP growth in Q1 2020, but it is still too early to say how strong would be the impact. This is rather unfortunate development as epidemic of coronavirus is happening right after we started to witness long awaited signs of recovery in global economic activity as measured by PMIs and OECD leading indicators. And unless situation in China is not stabilized during the upcoming weeks, recovery in global economic data may become only temporary and risks of global recession that we observed during late 2018 and 2019 would again reemerge.

Global PMIs vs performance of global equities

Source: Bloomberg

OECD total composite leading indicators vs global equities

Source: Bloomberg

However, for now there is probably still no need to panic. In best case scenario, if Chinese would manage to contain or at least significantly reduce spread of the virus in the upcoming month, strong relief rally in global equities is likely to ensue, as risks for future economic growth would be significantly reduced once again. Alternatively, if business activity in China would continue to remain paralyzed also in spring, impact on the global economy would be negative, of course, but it does not necessarily mean that prices of equities would significantly drop in price. Key reason is that global central banks would continue to inject liquidity in the financial system, and provide significant support and demand for asset prices.

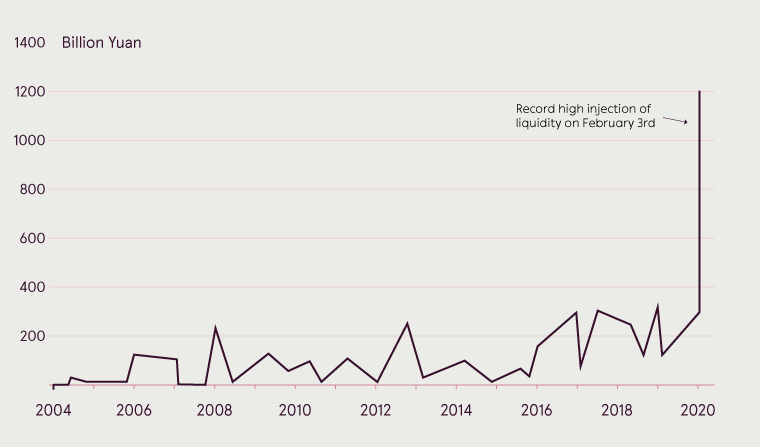

People’s Bank of China already poured record high $173 billion of funds into financial system after Chinese market was reopened from public holidays on February 3rd, and it is certain that more funds would be provided by monetary authorities, if there would be need to stabilize financial markets further. At the same time FED in USA also indicated that they plan to continue running their repurchase operations, buying treasuries from market participants, and thus providing extra liquidity to US banking system at least until April. So just as in 2019 when global macroeconomic indicators were deteriorating, but equity markets continued to increase in price, same situation might again be observed in the first half of 2020.

People's Bank of China Repo injection

Source: Bloomberg

And only in scenario, when coronavirus will get out of control in China and become a global pandemic, shutting down global trade and putting significant hurdles on business operations around the world, major crash in the markets can be expected. So far, risk of such scenario is rather low, and unless news from China would not worsen, any sell-off in equities should be considered more as a buying opportunity than as a motive for additional fear.

The impact of coronavirus on financial markets has so far been fairly moderate. Emerging market equities took the biggest hit and are down around 7% from their highs. World equity market (as measured by MSCI ACWI), however, is just about 3% lower than its all-time high. Actually, one can say that such correction was already well overdue, as ACWI has marched higher without at least 3% drop since the beginning of October 2019. Moreover, the correction has helped to clear excessive investor optimism that was prevailing in the market, and it is not a headwind to the equity markets anymore, but on the contrary should provide support going forward. For example, according to the American Association of Individual Investors (AAII) latest survey, the number of bullish investors dropped by almost 14 percentage points in one week to 32%. At the same time the number of bearish investors grew 12 p.p. to 36,9%. Still, investors have to be prepared to increased volatility in the near to medium term as many uncertainties remain.

1Formal designation of virus according to World Health Organization

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.