Navigating a turbulent global economy

- Banking sector in turmoil

- Central banks stay the course;

- Chinese economy shows signs of recovery

The spring has already started and with it comes the hope for calm after a chaotic 2022 that included the war, the energy crisis, soaring inflation and the fastest global central bank tightening cycle in decades. Not this March, though, as the turmoil in the banking system has knocked the confidence on the economic situation off‑the‑track and urged the market participants to re‑assess their projections, once again.

Mainly thanks to the concerns about the banking sector, the financial markets have been shaken over, but managed to recover till the end of the month, resulting in a 0.6 % increase of the MSCI World index (EUR). Better results were shown by the emerging markets stocks’ gauge MSCI Emerging Markets index (USD) that gained 2.7 %.

Banking sector under pressure

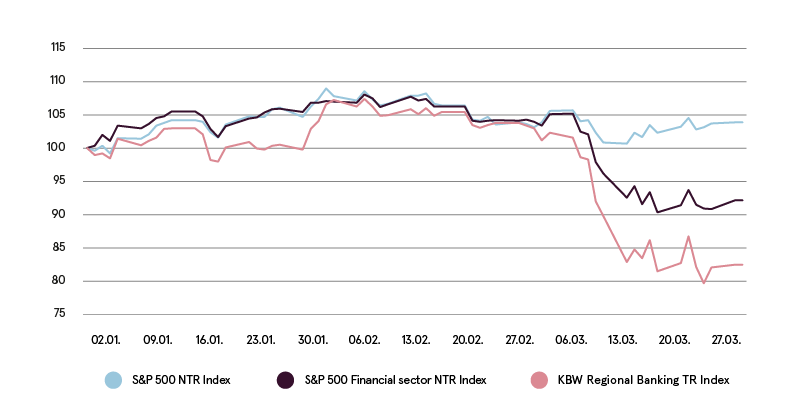

In the wake of the shock from the Silicon Valley Bank and Signature Bank (among others) failures, the primary focus is on the rest of the banks as investors evaluate the vulnerability of the banking system. The announcement that all depositors at the two banks will receive full reimbursement, alongside the Federals Reserve’s (Fed’s) newly formed bank lending program to provide funding for deposit‑taking institutions, provides a foundation of confidence in the stability of the banking system. Despite this, it is not yet certain that the situation is resolved as it will take time for the dust to settle before any secondary effects on the banking system can be accurately assessed. As a result, we have seen the financial sector, and particularly US regional banks, substantially underperform the broader market this year.

Financial sector has sharply underperformed the S&P 500 Index

Source: Bloomberg LP

Central banks grapple with new obstacles

As expected, in the last meeting the Federal Reserve raised interest rates by 0.25 %, bringing the Fed funds rate to 4.75 % – 5.0 %. During the meeting, the Fed delivered two messages that were equally important: one focused on combating inflation, while the other was centered around offering assistance to address the instability in the banking sector. Regarding inflation, the Fed is still using its monetary policy tools to decelerate economic activity. Some members of the board believe the Fed may be closer now to the end of its tightening cycle. On the banking crisis, the Fed is prepared to employ its liquidity tools as necessary to provide support for the banking sector. This may include emergency lending and increasing the flow of funds to enhance the liquidity. In any case the Fed maintains its belief that the US banking system is strong and capable of withstanding the challenges.

In the middle of the month, we also saw the European Central Bank (ECB) raising rates by 0.50 % and noting they would remain data‑dependent when determining the path of the rate hikes going forward. However, the recent turmoil in the financial markets has made the path ahead less certain. The Bank of England pushed ahead with another 0.25 % interest rate increase, as well, focusing on its ongoing inflation battle.

Chinese economic data shows recovery

According to the Chinese economic data, there are indications of a recovery, as industrial output has increased by 2.4 % from the previous year. However, this is slightly lower than the anticipated rate of 2.6 %. Chinese authorities have committed to provide extra liquidity to support economic expansion. After lifting strict COVID‑19 restrictions at the end of the last year, Chinese authorities have reopened the economy, enabling consumers to travel and re‑commence spending on services (Retail sales rose 3.5 % in January and February compared to the same period last year), while also adding to the manufacturing capacity. Moreover, China has encountered remarkably low inflation levels and policymakers are likely even trying to prevent the deflationary pressures. That posts the contrasting picture, as the inflation across most of the world has been far higher than policy makers are comfortable with.

House View update

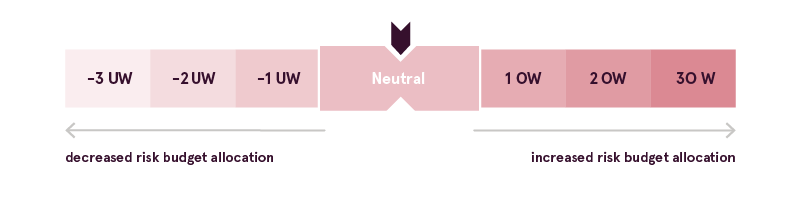

In response to the ongoing market volatility, we are taking a wait and see approach in this turbulent environment. We decided to retain the neutral risk allocation budget, while closely watching the latest developments. Overall, instability and defensive posturing may persist for a while, as the confidence in the banking sector may take time to fully return.

Luminor House View

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.