Pessimism is in the air, but reasons for hope still remain | Luminor

Pessimism is in the air, but reasons for hope still remain

- Equity markets dropped in August as trade war between USA and China has intensified;

- Upside in September to large extent would depend on more stimulus announced by central banks and potential trade talk improvements;

- In the long term, equities are clearly more attractive than bonds; however, both equities and bonds may experience significant volatility in the near to mid-term

After relatively quiet July, August turned out to be rather rich month both in terms of events and price movements. In the very beginning of the month, equity markets experienced real panic as prices of global indexes on average fell by more than 5% in less than a week. Such drop was triggered by new tariffs announced by USA towards China, and realization that trade war is likely to escalate going forward, as both countries seem to be unwilling to find compromise, despite some of their statements made previously.

Indeed, later during the month, more negative statements by both countries have followed. China announced that as a retaliatory measure to new US 10% tariffs on $ 300 billion of Chinese goods it would also introduce 5-10% tariffs on $ 75 billion of US imported goods, including commodities such as soya beans and crude oil. Trump reacted to Chinese news almost immediately, tweeting that new 10% tariffs would be raised to 15% and existing 25% tariffs would also be raised to 30%.

In parallel to blaming Chinese, Trump was also very harsh in relation to FED, at one time even asking if Chairman Powell is the bigger enemy to US interests than Chinese president Xi. Major reason for Trump’s concern, is that USA right now has one of the highest interest rates among all developed countries in the world.

Interest rates in developed countries

| Hong Kong | 2,50% | United Kingdom | 0,75% |

|---|---|---|---|

| United States | 2,25% | Eurozone | 0,00% |

| Canada | 1,75% | Japan | -0,10% |

| Australia | 1,00% | Sweden | -0,25% |

| New Zealand | 1,00% | Switzerland | -0,75% |

Global economic slowdown and weakness in some leading US macroeconomic indicators, indeed, point to possibility that first interest rate cut in 11 years implemented by the FED in the end of July might not be enough. And if FED continues to be reactive, as it did in 2000 and 2007, Central bank might again be too late to prevent recession, as local companies would not be able to get stimulus when it would be needed the most.

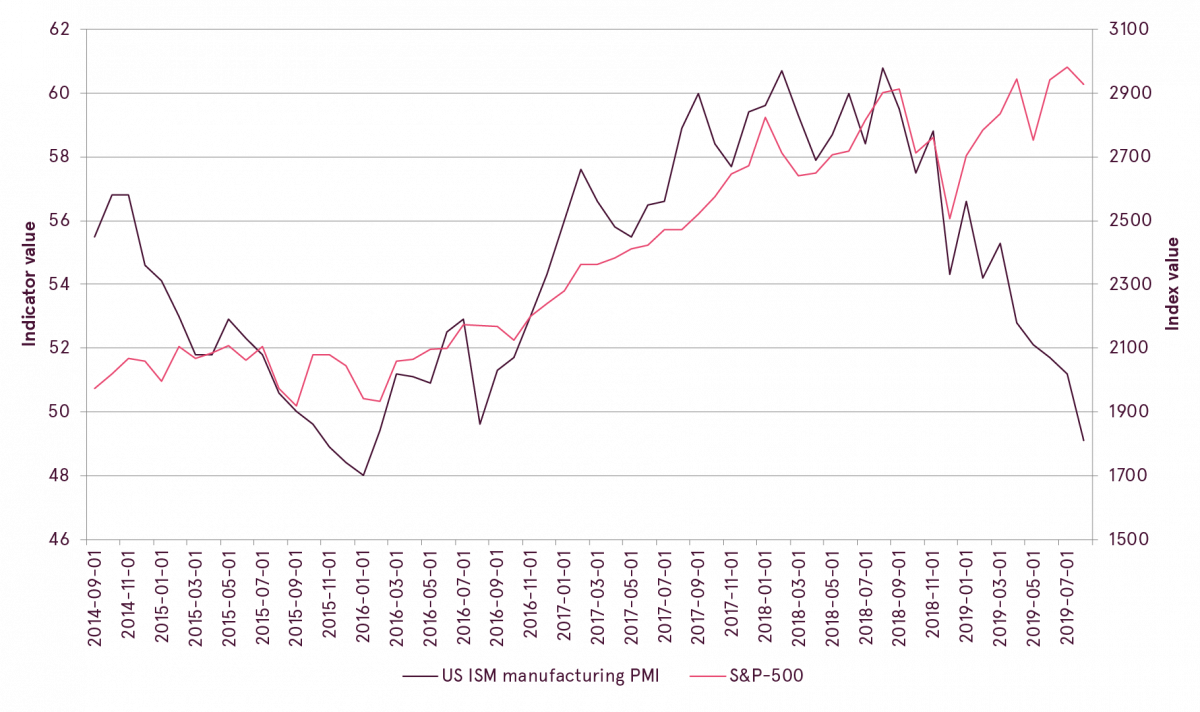

US PMI vs global PMI

Another channel through which high interest rate may potentially hurt US economy is through rising US dollar. For already 1.5 years dollar is trending higher as more investors in search for yield find US assets to be more attractive, especially given that US economy is still holding relatively well compared to vulnerability elsewhere around the globe. High dollar makes exporters less competitive and also may lead to lower revenues realized by large multinational firms, as they receive large share of their income from abroad. So if appreciation of USD continues going forward, it might become a serious issue for USA indeed.

US Dollar index

In addition to US related issues, news from other countries were not particularly bright either. Negative GDP print in Germany for second quarter 2019; rising chances of hard Brexit in UK as newly elected Prime Minister Boris Johnson seems rather determined to make no deal with EU, unless terms become more favorable for the UK; and short-term government crisis in Italy as break down of existing coalition and resigning of prime minister raised new concerns about political risks in Europe – all these factors led to additional rounds of uncertainty throughout the month.

Also it is worth mentioning development in Argentina. First round of presidential elections led to surprising results as populist, left wing candidates gained majority there. As a result Argentine stock market dropped by 48% in one day, which according to Bloomberg is the second biggest one-day drop in 70 years experienced by any country. And though Argentina does not have much impact on global affairs, it proves the point that we are operating in quite nervous times.

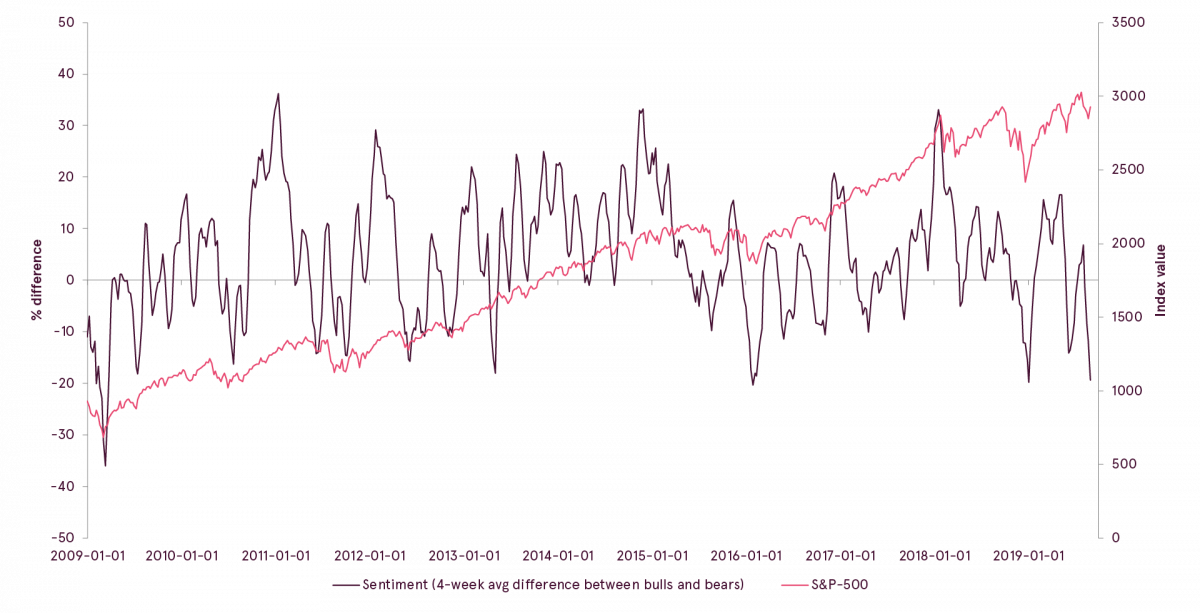

Not surprising, that given rather negative background, majority of investors were becoming more and more pessimistic throughout the month. As a result, by September some sentiment measures became rather extreme in terms of where investors believe the markets are headed next. For example, difference between bullish and bearish investors as measured by US AAII sentiment survey approached similar level as in late December 2018, which coincided with major market bottom. Furthermore, if we take 4-week average of such readings (as a proxy for average sentiment throughout the month), the only other time when there was more pessimism during last 10 years was February 2016, which was yet another major market bottom.

AAII investor sentiment vs S&P-500

At the same time, despite all the pessimism and aforementioned news items, equities held relatively well throughout the august after initial decline early in the month. Moreover, if we exclude first three trading sessions in August, results for the rest of the month would actually turn out to be positive. This is indeed surprising, as usually we should expect much stronger drop in equity prices given sentiment and level of risks. So what positive factors still continue to support the market and prevent it from falling further?

First of all, there is good chance that USA and China would again become softer towards each other and will be able to resolve existing disagreements. Subtly we can see that both parties are still willing to find the solution.

For example, on September 1st new tariffs were introduced only for about $ 110 billion out of planned $ 300 billion of Chinese goods, while the rest impact was postponed until the mid-December. At the same time, Huawei, which also was expected to receive full ban on doing business with US companies in August actually received another 90-day delay until the November. Move by Chinese which imposed smaller tariffs of only 5 to 10% and also postponed large part of it till December also may be considered as forced measure, in order not to look completely weak, but that country is still willing to resolve issues with USA.

Next, in middle September there would be another ECB and FED meetings, where both banks are expected to cut interest rates further. Hard to judge how financial markets would react to these events, but if some additional stimulus measures would be announced, price movement may turn out to be quite bullish, just as it already happened several times earlier this year.

Finally, if majority of investors right now are bearish, they have already most likely acted on their view and there are not many sellers left in the market. Few good catalysts might return appetite of the bulls, and at least for a while there might be decent technical bounce.

On the fixed income side, however, the situation is the opposite, as very optimistic investors have driven the prices substantially higher. Interestingly, with over 16.8 trillion USD of bonds with negative yields, many investors are buying bonds with the expectation of capital appreciation, not yield income. As a result, the aggregate global bond index provided a return of around 12% in the first eight months of this year, compared to the average annual return of 4.3% over the last 20 years. The move can be explained by the very aggressive expectations of rate cuts from major global central banks.

Although, considering the economic slowdown and tame inflation, the prospects of lower interest rates ahead are very high, too aggressive rate cut expectations pose a risk of potential disappointment. Should the central banks fail to deliver according to investor expectations at their next meetings, investors may be forced to reprice their expectations, potentially causing higher volatility in bond prices.

Forward P/E*

| Current | |

| Developed Markets ex US | 13,2 |

| All Country World Index | 14,8 |

| Europe | 12,8 |

| Emerging Markets | 11,6 |

| USA | 16,8 |

* price divided by the 12 m forward earnings estimate

Source: Yardeni Research, Inc.

From the valuation perspective, global equities continue to be fairly reasonably priced, with the US being more expensive and emerging markets relatively cheap. Moreover, lower interest rates should support the increase in equity valuation going forward by reducing the cost of capital. At the same time, current valuation is dependent on corporate earnings growth rebounding by the end of this year, which heavily depends on improvement in the global economy. Should the world economic growth take longer to recover, equity markets may come under pressure in the short term.

All in all, our view is currently rather balanced: in the long term, equities are clearly more attractive than bonds; however, both equities and bonds may experience significant volatility in the near to mid-term.

OECD total composite leading indicators vs global equities

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.