Entering 2021 – hopefully more relaxed, but possibly more challenging year than 2020 | Luminor

Entering 2021 – hopefully more relaxed, but possibly more challenging year than 2020

- 2020 was challenging year as both positive and negative extremes have materialized; 2021 risks to become not any different;

- Impact of vaccinations on COVID‑19 trends, political events in USA and new earnings season – these are the factors to watch in January as they can provide hints for further 2021 results.

A year ago when we were trying to give prediction on what can happen in 2020, we indicated that it is “complex year for financial forecasting, as…there are good reasons for 2020 to turn out as either extremely good or extremely bad year for investments.” We mentioned that if global economy remains in good shape and central banks continue to provide stimuli - “investor euphoria that has started in 2019 might reach rather extreme levels, and equities will be capable to experience parabolic rise, even if rationally there are no sound logic for such development”. We also mentioned that “majority of risk factors that were present throughout 2019 still remain, and thus economic recession and crash in the financial markets cannot be ruled out”1 .

So it turns out, we were correct when we expected possibility of extreme outcomes2, however, what we were not able to imagine and what also made investment process last year so complicated and unprecedented compared to all other years is that both extremely positive and negative scenarios were able to materialize in 2020 all at once.

When in March financial markets started to crash, it became crystal clear that world is entering deepest global recession since 1929 Global Depression (thus negative scenario), with parts of economy becoming paralyzed (e.g. hotels, airlines etc.), workers being laid‑off en masse and many companies experiencing at best significant decline in earnings and at worst risk of going out of business.

We acknowledged that fiscal and monetary stimuli could bring short‑term economic relief, but given that 2020 damage is so severe and that it takes considerable time to fully restore business activity to sustainable pre‑crisis levels, in spring we did not expect financial assets to fully recover in value to pre‑COVID levels anytime soon. We also had to abandon possibility of most positive scenario, mentioned last January, as record high investor optimism and speculative manias have never happened in times of struggles and hardship for so many people involved.

But 2020 proved us wrong, as processes, which previously seemed to be impossible to happen, actually have materialized. After one of the most significant and fastest declines ever, since late March 2020 risky assets also experienced one of the strongest rallies on record with various indices making new all‑time highs in less than six months from their March bottom.

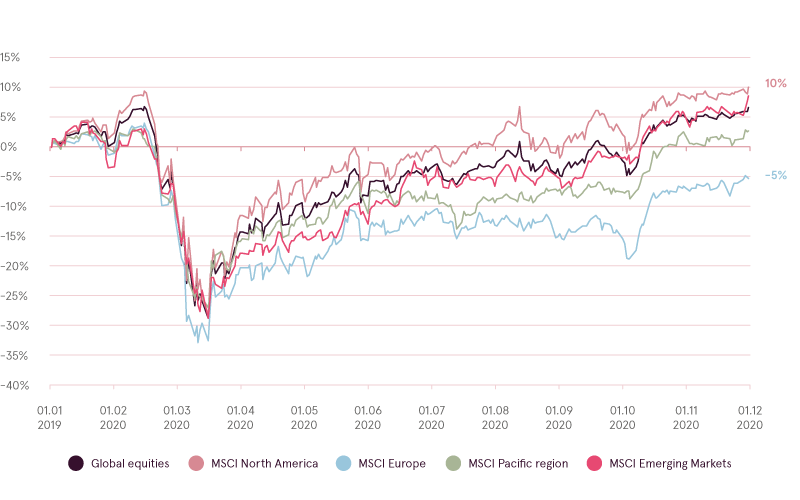

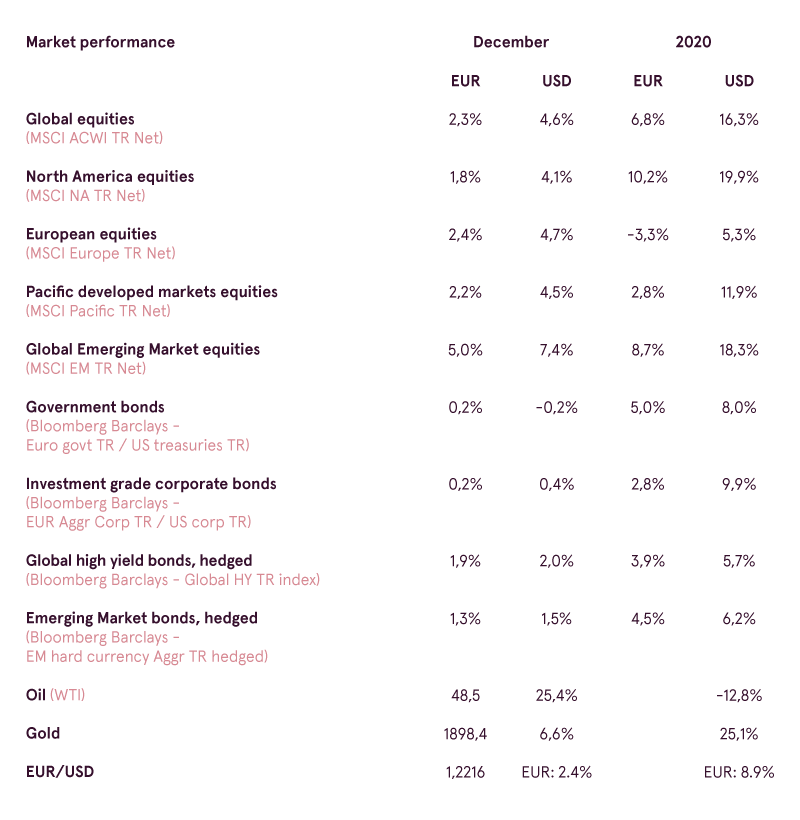

Net performance of regional equities in 2020 (EUR)

Source: Bloomberg

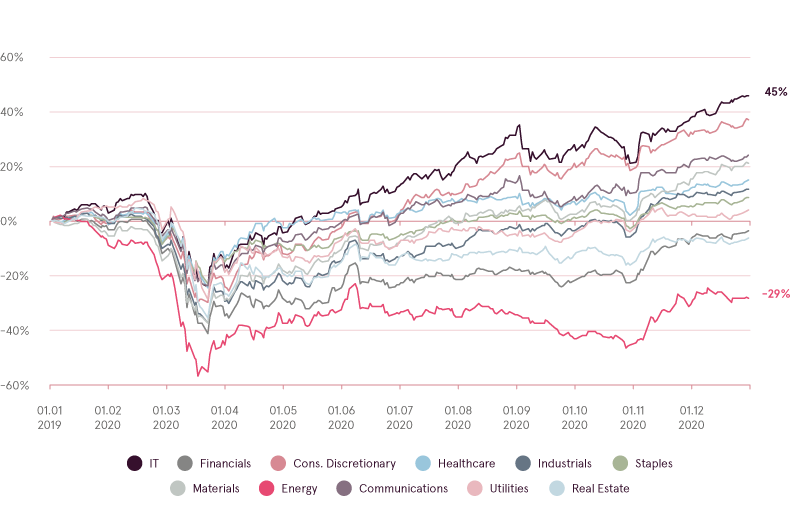

Net performance of equity sectors (EUR)

Source: Bloomberg

Big question now is what will happen in 2021. Though it is very tempting to say that given magnitude of events last year, 2021 probably will be calmer and less volatile period, however, in reality, it may turn out far from true. Challenges that financial markets are facing right now are much more severe than a year ago, and the best prediction for 2021 is probably to say that literally anything can happen and the moves could be even more significant and extended than last year.

Let’s say vaccines are working and COVID‑19 is gone, at the same time government and central banks still continue to inject fiscal and monetary stimulus. Economy recovers to pre‑COVID levels or even higher, and companies are able to show strong earnings growth. Inflation expectations continue to rise while real yields thanks to monetary policy remain negative. Meantime unemployed and small business owners continue to receive support from government and aggregate population income is higher. More and more people start to invest with desire of strong and fast gains like already happened in assets like Tesla or Bitcoin and also of fear of higher inflation. Participation in stock market becomes much wider, potentially leading to even more significant speculative mania and creating major “bubble”. In 2021 such scenario is not so unrealistic; at the same time, it means that equity gains could be as much as 50%+ this year (equivalent to their 2020 price increase from March bottom until the year end).

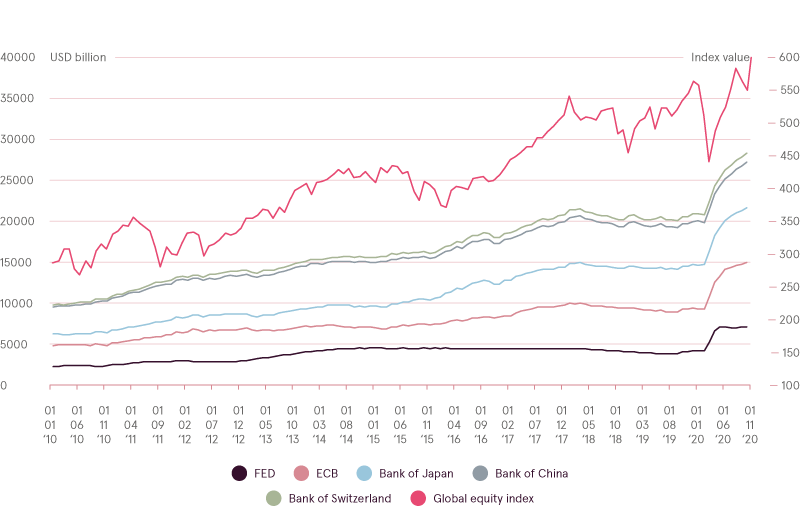

Major central bank total assets (USD'bln) and performance of global equities

Source: Bloomberg

But let us imagine another scenario, where COVID‑19 still remains major issue throughout the year and businesses continue to get closed with unemployment rising. Banks continue to resist new lending and new fiscal stimulus is limited due to political and taxpayer tensions. Population income is falling and deflation becomes a major threat. Companies are unable to return to pre‑COVID levels of profitability and economic recovery is either slow or non‑existent. Meanwhile equities are at record high valuation levels, and given negative economic outcomes more and more investors realize that fair value of companies should be at much lower prices. Major and more significant correction than in March 2020 would ensue. Variation of such scenario with major decline in asset prices is also quite realistic. In fact, if there would not be government support throughout 2020 that is what would have already happened last year.

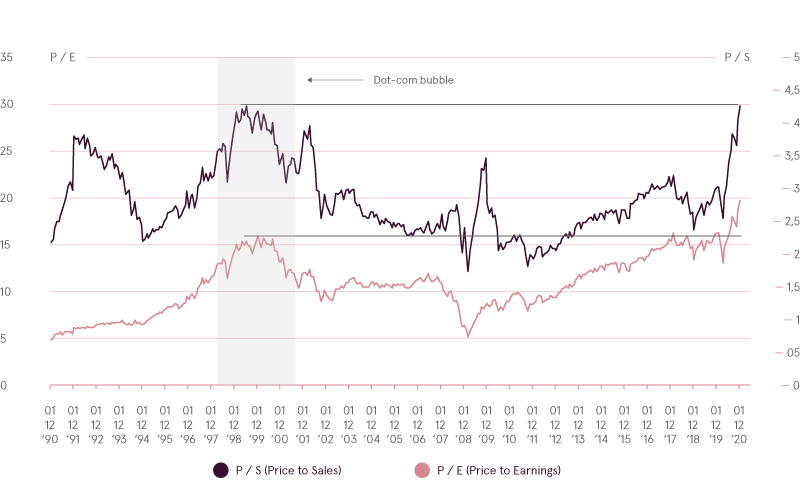

Key valuation metrics of S&P‑500

Source: Bloomberg

Hopefully, neither of aforementioned extreme scenarios would materialize and we would see much more moderate outcome this year. But given 2020 events and current market environment we have to be prepared for both of extremes. Good news is that much more clarity of what to expect this year can be achieved already in January.

First of all, vaccination process has already started and millions more would be vaccinated by the end of the month. Hopefully, in the upcoming weeks it would allow to evaluate, if negative trends in disease spread are starting to be reversed, so that lockdowns could be ended in the nearest future.

Secondly, Joe Biden will be inaugurated as a new US president on 20th of January. In addition, on 5th of January democrats won senate elections in Georgia and thus got majority in senate, meaning that they will be now in control of both houses of Congress as well as White House, untying them to pass any legislation they want. By the end of the month we would likely get first glance on Joe Biden and democrats’ action plans on what they are willing to accomplish (e.g. higher taxation, fiscal stimulus etc.) this year and what can be implications for the stock market from it.

Thirdly, earnings season starts in mid‑January and it would be crucial to understand if companies still were able to improve their financial results in last quarter, despite new lockdowns and some regional economic weakness. Finally, we may get some macroeconomic hints in relation to $900 billion stimulus package and $600 checks distributed to each person in the end of December in USA. Key question is whether such support was enough for those that are in need or macroeconomic data would show that even more aid is needed to prevent return of economic recession.

1Please refer to January 2020 market update

2Though factors which brought those outcomes were slightly different, COVID‑19 was still not known at that time

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.