With markets cooling off, US politics and COVID‑19 developments come into spotlight | Luminor

With markets cooling off, US politics and COVID‑19 developments come into spotlight

- Strong reversal in prices of certain financial assets in early September indicate that equities might have entered consolidation period

- Potential passing of new fiscal stimulus bill in October and presidential elections in early November in USA could have material short‑term impact on prices of global financial assets in both directions

- Coronavirus cases continue to rise, and if trend is not reversed, new lockdown measures could be reintroduced globally

- Upcoming “event risks” suggest that high volatility is likely to persist

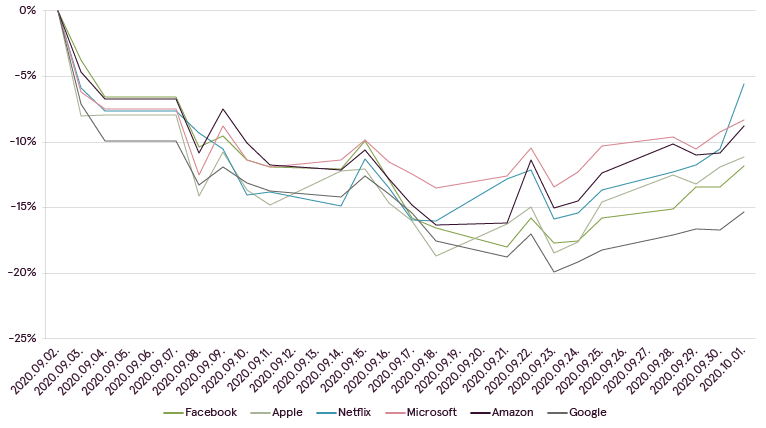

In September equity markets finally took a pause to ongoing rally, with majority of global equity indices falling in price during first month of autumn. Last time we mentioned that certain equities were rising inadequately high and fast in August, reminding us of patterns observed during speculative mania. Therefore, it was not really a surprise when these stocks experienced strong reversal in the matter of days with declines from peak to trough reaching 20% to 35% depending on the particular stock selected. As already discussed, such sharp moves in largest and well established companies cannot be considered reasonable and actually serve as a reminder that despite recent strength financial markets still remain relatively fragile.

FANMAG performance in September

Source: Bloomberg

Such fragility can be explained by the fact that without support of governments and central banks, large number of companies would experience massive financial difficulties and risks of becoming insolvent. Even with financial aid in place, companies still experienced significant decline in their financial results this year. According to Refinitiv data, during second quarter 2020 earnings and revenues of US S&P‑500 companies dropped by 31% and 9% respectively, while drop for European Stoxx600 companies constituted - 51% for earnings and -20% for revenues. Until the end of the year such figures are expected to improve somewhat though still remain negative. Expectation is that only next year companies would be able to recover fully and show decent growth in financial performance.

S&P and Euro stocks revenue and earnings growth and growth estimates

Source: Refinitiv

In our view, there are considerable risks that even such positive expectation may not materialize, if support is being removed. Usually, when there is economic recession, like this year, most indebted and uncompetitive companies go bankrupt, removing economic excesses and making financial system healthier. However, this time around, such inefficient companies still remain afloat as they have access to cheap and highly available financing through financial markets or through funds granted to them directly by governments. Therefore, supply of goods and services is not being considerably reduced right now, as it has always happened in recessions before.

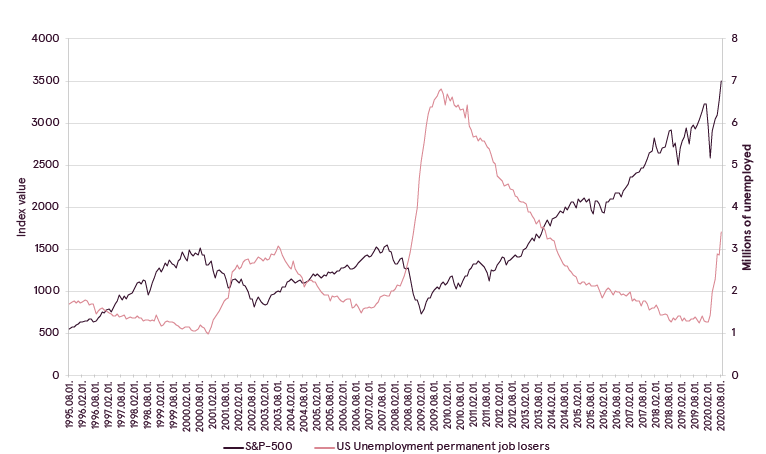

At the same time demand during recessions usually is being reduced through higher unemployment and adverse consequences that it has on personal income and spending capabilities. Indeed, right now we actually see excessively high unemployment rate across the globe with permanent job losses in USA continuing to surge on pace with previous 2008 recession. However, due to increased unemployment benefits and direct payments to population by the governments no significant decline in income and therefore demand is experienced yet.

S&P‑500 performance vs US permanent job losses

Source: Bloomberg

From all this follows interesting observation – while governments keep supporting producers and consumers, demand and supply remain relatively elevated for the time being, providing impression that economy is going back to normal. Post‑COVID improvements in macroeconomic data to large extent support such feeling, and therefore market participants are largely optimistic about future economic growth. Big question, however, remains – what would really happen, when financial aid is finally gone? In that case consumption is likely to drop, leading to lower demand, followed by excess supply, lower revenues and profits for corporations, and if financial markets are rational also decline in asset prices. Partially market decline in September supports such logic, with no new stimulus measures announced and already allotted funds coming to an end, “fuel” for further macro improvements and rally in asset prices is also coming to an end.

Understanding these threats, democrats and republicans by the end of September decided to resume negotiations to pass new stimulus bill. Parties cannot yet reach agreement on the amount of funds, but, anyway, if passed, total size of stimulus would be almost certainly more than USD 1 trillion. This is extremely large amount of money, and most likely short term consequences of such bill being passed would be positive for the markets and the economy, so we may see yet another rally in risky assets for at least another 3‑6 months. It is also expected that bill may include another round of USD 1,200 checks to population, and if just like in spring, part of this money is spent on trading in financial instruments, it may also prolong speculative excitement that has been witnessed in certain stocks recently and lead to new price records.

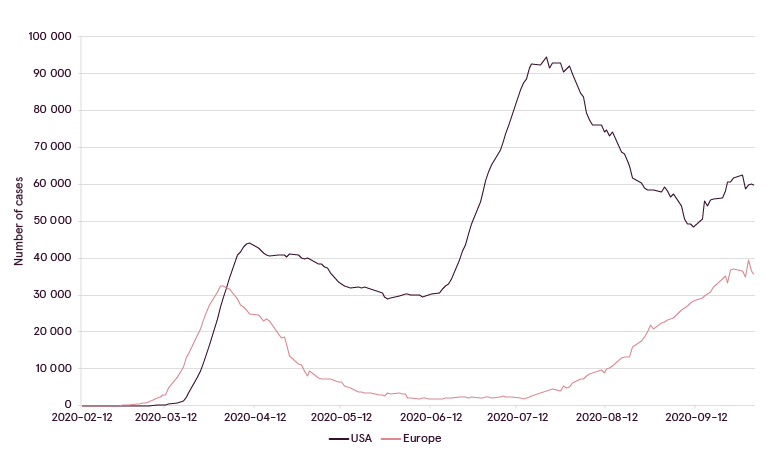

Meanwhile coronavirus developments are again taking central stage. Number of new cases continues rising steadily all across Europe, raising concern that new widespread lockdown measures could be introduced similar to how it happened in spring. Cities, such as Madrid, for example, where situation is especially challenging, have already reintroduced lockdown measures, and other hotspots across Europe may follow soon thereafter. In USA also after gradual decline in August, COVID‑19 new cases started to rise gradually in mid‑September, and on 1st October major headline was announced that Donald Trump has contracted coronavirus.

COVID‑19 USA and Europe cases

Source: Bloomberg

With less than one month left until US presidential elections, Trump testing positive for COVID‑19 adds another layer of unpredictability to market behavior both before and after the elections. Seasonally, it is usually the case that stock market tends to experience worst declines during the election year just 1 month prior to new president being selected, so precisely in October. Overall, such market behavior is rather reasonable, as investors do not want to risk their profits and participate in potential volatility, if not their “favorable” president is being selected. This time around it is really hard to say, victory of which presidential candidate would be more beneficial for financial assets, and what can be initial market reaction to victory of one or other nominee. Last time many thought that stock market would tank, if Donald Trump would be elected, but in reality markets barely noticed and actually made new all‑time high just around one week after he had won. This time polls so far indicate that Joe Biden has better odds of becoming a president, and given his stance on increasing taxes for corporations and high net worth individuals, initial market reaction to his potential presidency might not be taken positively.

US presidential elections 2020 average poll results

Source: Bloomberg

However, most likely irrespective of who wins US presidential elections, more important factors determining future market direction at least this year would be linked to situation with COVID‑19, direction of macroeconomic trends, central bank actions and availability of new government stimuli. In that sense, both candidates likely wouldn’t have much power and influence to impact how these things are progressing.

Given that market reaction to certain upcoming events, like passing or not passing of fiscal stimulus bill in USA; coronavirus progression and how well Trump overcomes the disease, what would be election results and how these results would be perceived by investors – persistence of high volatility in financial markets is highly probable. Navigating such markets requires prudent long‑term planning and keeping the portfolio consistent with one’s risk tolerance.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.