Stock market excitement intensified in August, but is it reasonable? | Luminor

Stock market excitement intensified in August, but is it reasonable?

- Investor mania in relation to largest and most popular US stocks intensified in August, driving S&P-500 to new all-time high. COVID-19 improvements and FED inflation remarks might have helped to fuel more optimism;

- Strength in US indices is not supported by other regions where performance remains sluggish, more adequately reflecting economic reality observed in 2020;

- Focus on longer term investment process over possibility of shorter-term speculative gains should help cope with volatile and risky market;

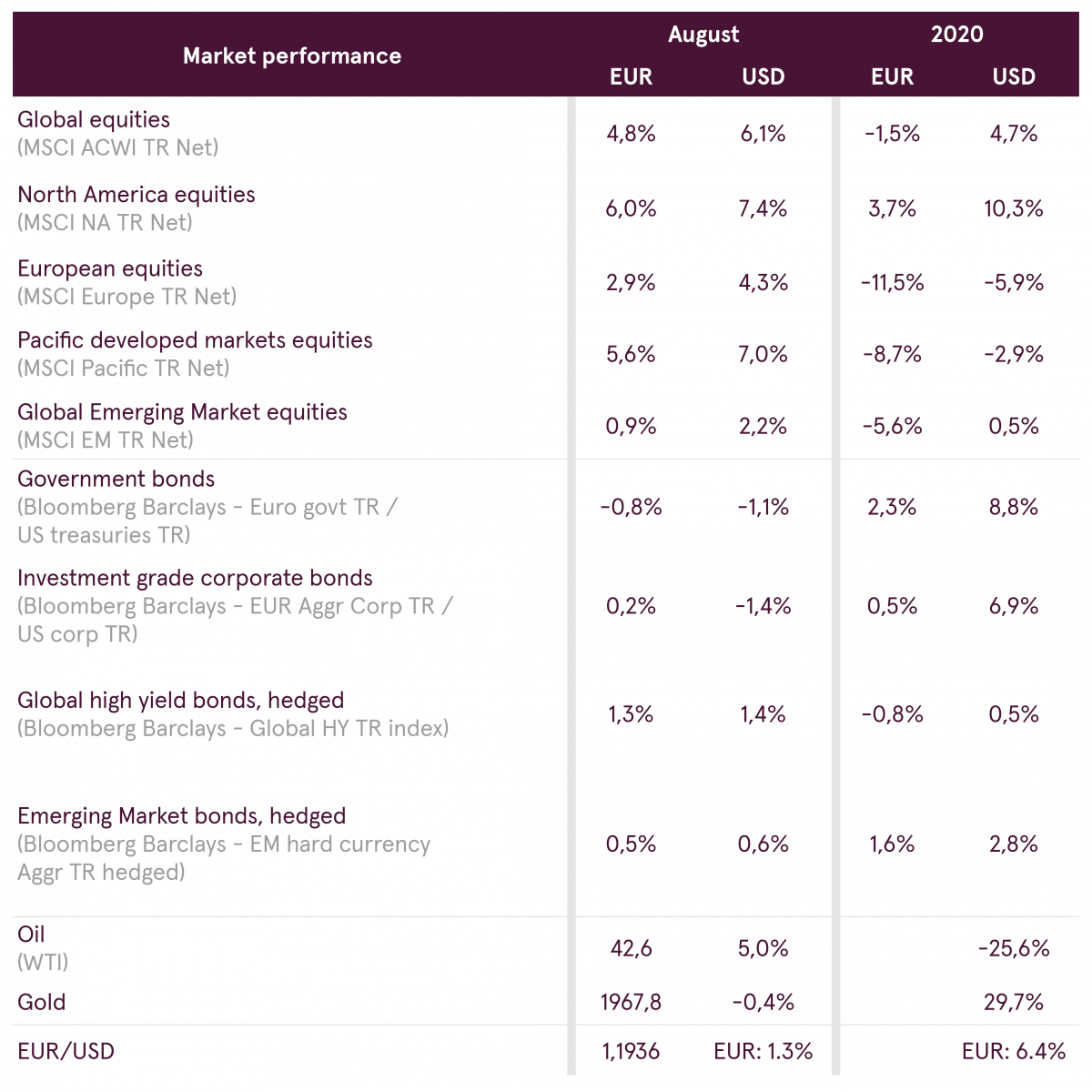

August was another positive month for equity markets as investor euphoria towards largest and most popular equities in USA only intensified, while US Central bank announced major policy shift towards higher inflation, and thus potentially towards creating even more liquidity, if that would be needed. In addition, contrary to Europe, number of new COVID-19 cases in USA started to decline. As a result, all these factors helped to propel S&P-500 index to new all-time highs and widen discrepancy in performance between USA and the rest of the world.

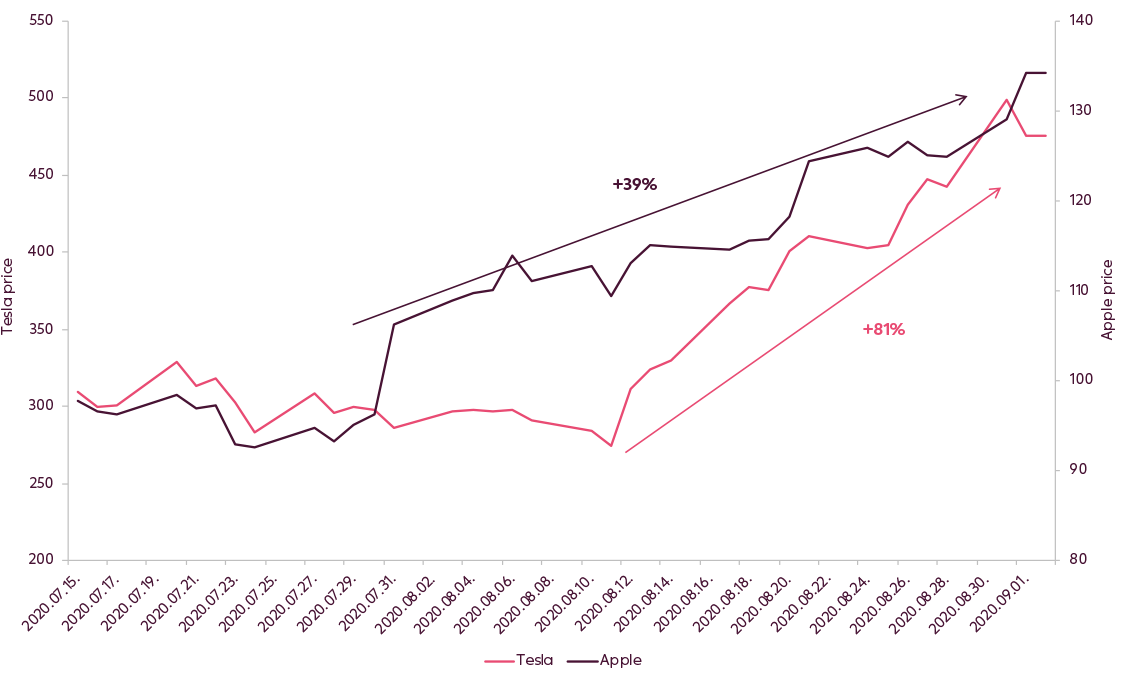

Last time we already mentioned that investor sentiment towards FANMAG1 stocks and Tesla is reaching rather extreme levels and hardly can be justified by future growth levels or other fundamentals. In august we received even more evidence of such euphoria. When $250 billion company rises by more than 80% in three weeks on no particular news and largest company in the world goes almost 40% higher since late July to reach market capitalization of 2.2 trillion2, there is no need to be investment professional to understand that such moves are almost certainly driven not by rational investment process, but predominantly by speculation and mania.

Performance of selected stocks

Source: Bloomberg

In general, manias happen very rarely and probably one of the most recent and well-known occasions of similar behavior could be linked to bitcoin price surge during late 2017. It is true that during mania stage it may be relatively easy for participants to enrich themselves, as price dynamics is going only in one direction and change happens incredibly fast. But, from longer term investment perspective, it quite often does not pay off to participate in such ideas, as price changes are not driven by rational market factors, but by short term excitement and greed on the assumption that there would still be more buyers than sellers in the future. Therefore, investors who decide to participate in manias, in essence, become transformed to speculators and start playing “guessing game”, which for majority of participants in the end also becomes a losing game, as reversals tend to happen even faster than price increases, making what for the long time appeared to be profitable position immediately unprofitable3.

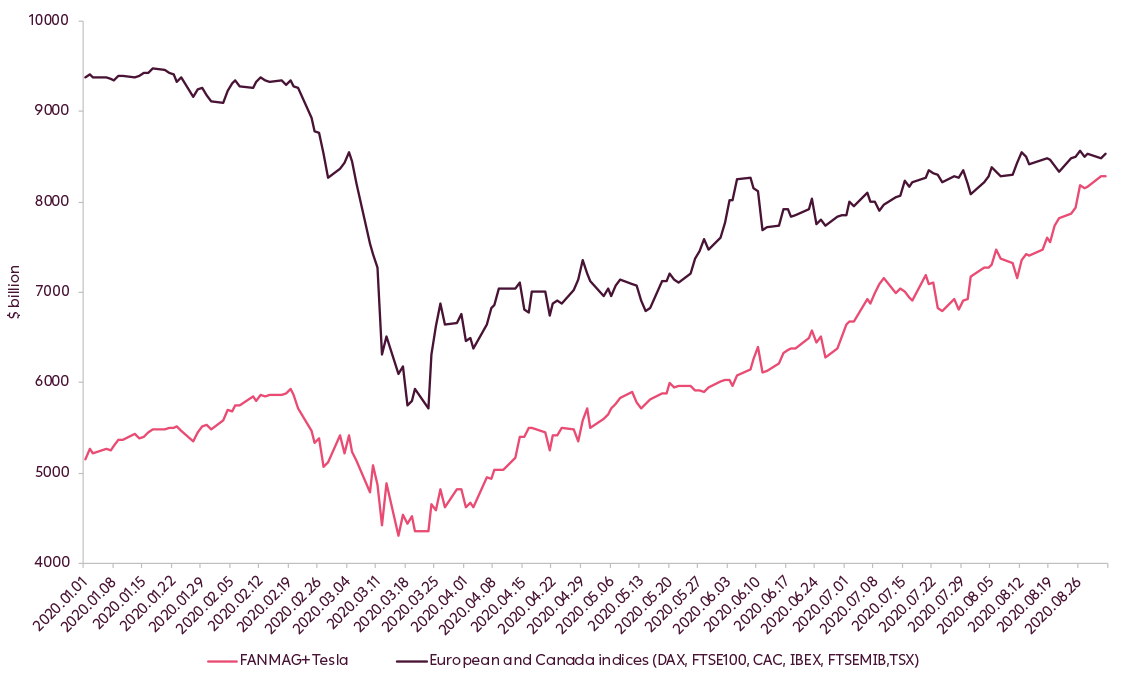

Capitalization of selected equities vs combination of selected indices

Source: Bloomberg

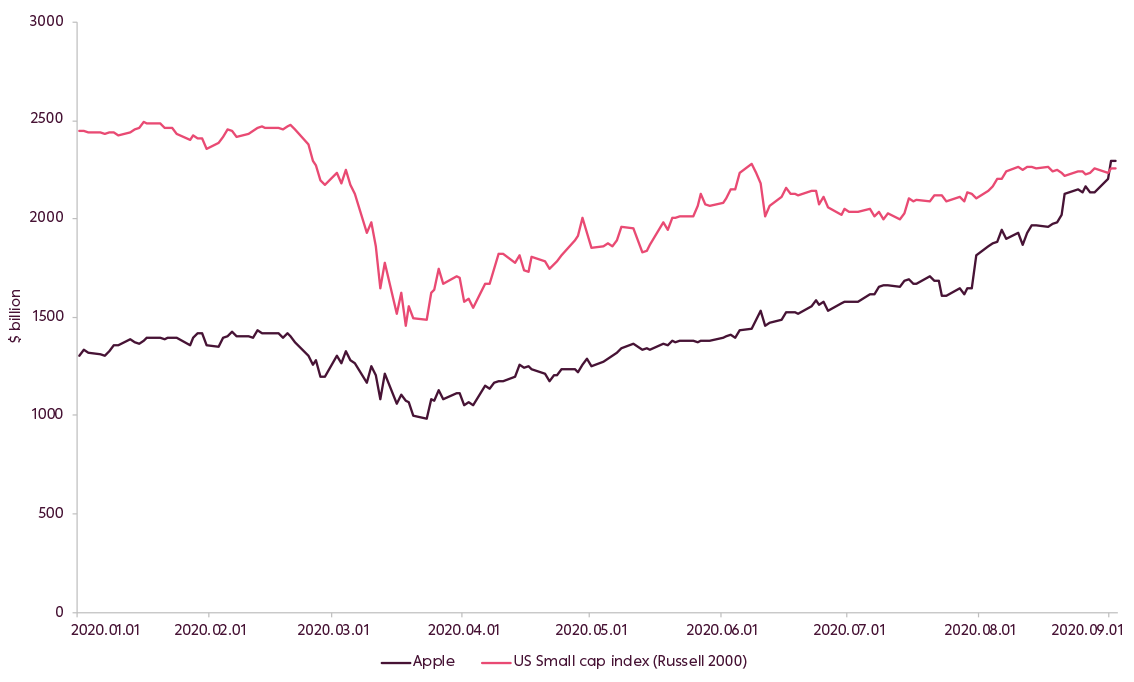

Capitalization of Apple vs US small cap index

Source: Bloomberg

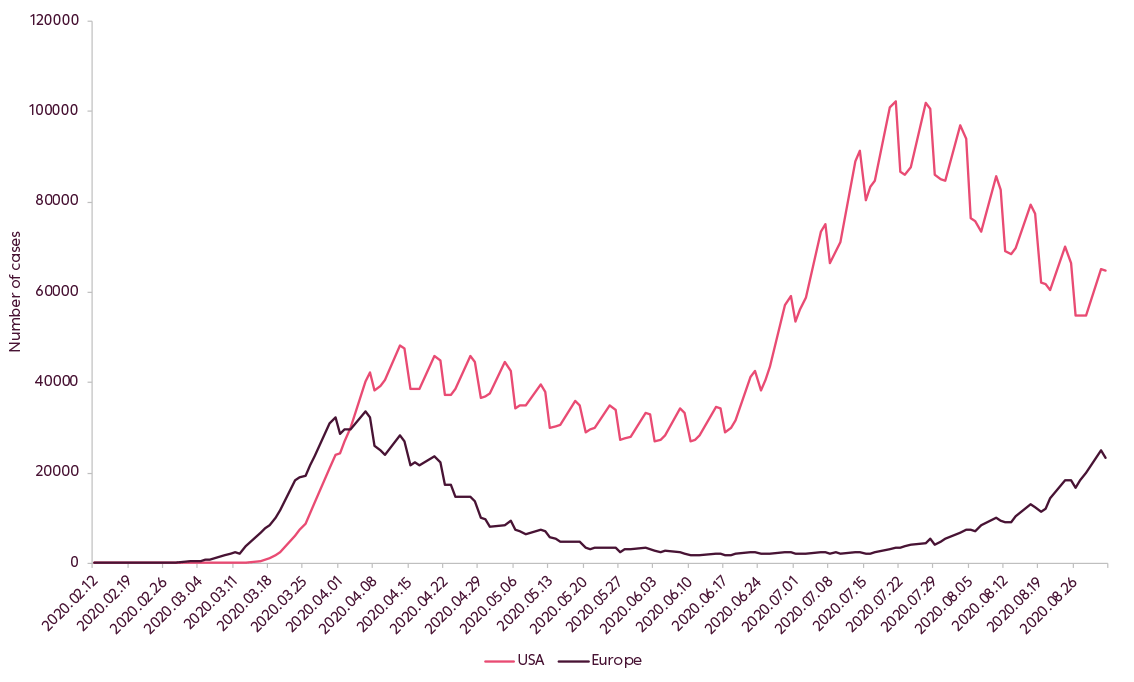

To be fair, mania in certain stocks was not the only factor that contributed to positive performance of indexes. Steady decline in new COVID-19 cases in USA allowed confirming that second wave has likely ended there even without strict shutdown measures this time. It is encouraging and allows cautiously to suggest that worst might be over if not from perspective of future public health developments, then at least from perspective of business closures and lockdowns. Also in late august FED chairman Jerome Powell announced that FED will no longer target to have 2% inflation and in order to create jobs and GDP growth may pursue higher inflation targets. Though, such message does not have immediate impact on monetary policy, it still seems to send encouraging signal for investors, that FED is willing to increase money supply even further, if situation would require such action.

New daily cases of COVID-19 (7-day average)

Source: Bloomberg

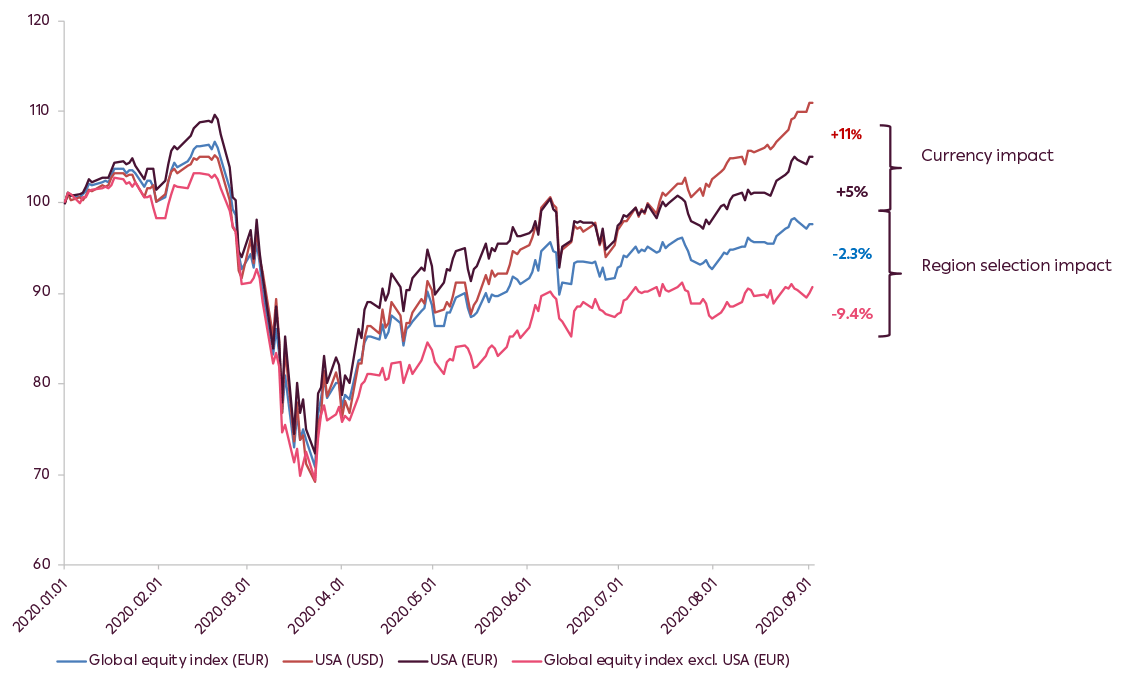

However, right now it is important also to differentiate between investor located in USA and investing only in local market against investor located in Europe and investing in global context (our case). Records in USA come with the price. By substantially increasing monetary supply, which contributed to equity prices going higher, FED at the same time triggered substantial decline in US Dollar. Since middle May US dollar declined to Euro by more than 10%. Additionally, spread between equity returns in USA and rest of the world since the beginning of the year widened to around 14%. In EUR terms, performance of global equities excluding USA since the beginning of the year is still around -10%, which in our view, more adequately resembles global economic situation that is observed in 2020, when not influenced by euphoria and investor mania.

YTD price return of selected MSCI indices

Source: Bloomberg

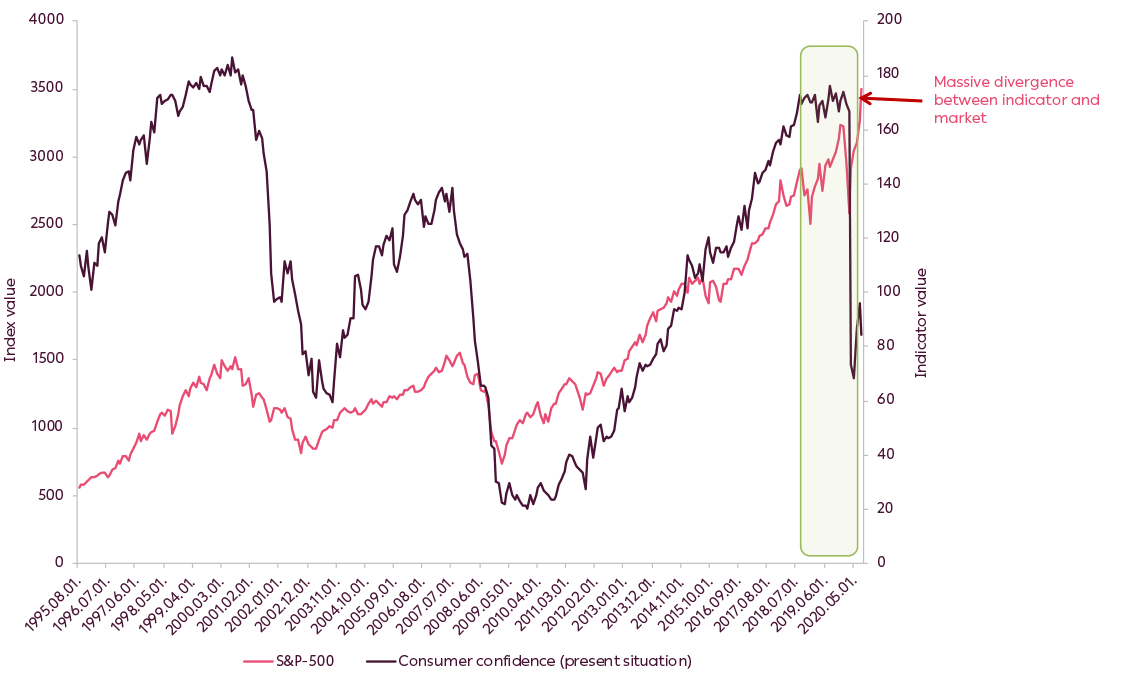

Global economic situation indeed remains challenging. While majority of macroeconomic indicators show improvements when measured on a month over month basis, almost all of them still remain below their respective levels observed last year. It still remains not clear how new increase of COVID-19 cases in Europe would impact economic activity inside this region in autumn. It is also not clear what would be macroeconomic data in USA after democrats and republicans failed to agree on new stimulus bill in August. Indirectly, we already see some signs of potentially weaker consumption going forward, as judged by consumer confidence data. And as you can see from the chart, such data almost always means trouble ahead for equity markets. 2020 in that regard is truly exception.

S&P-500 performance vs consumer confidence

Source: Bloomberg

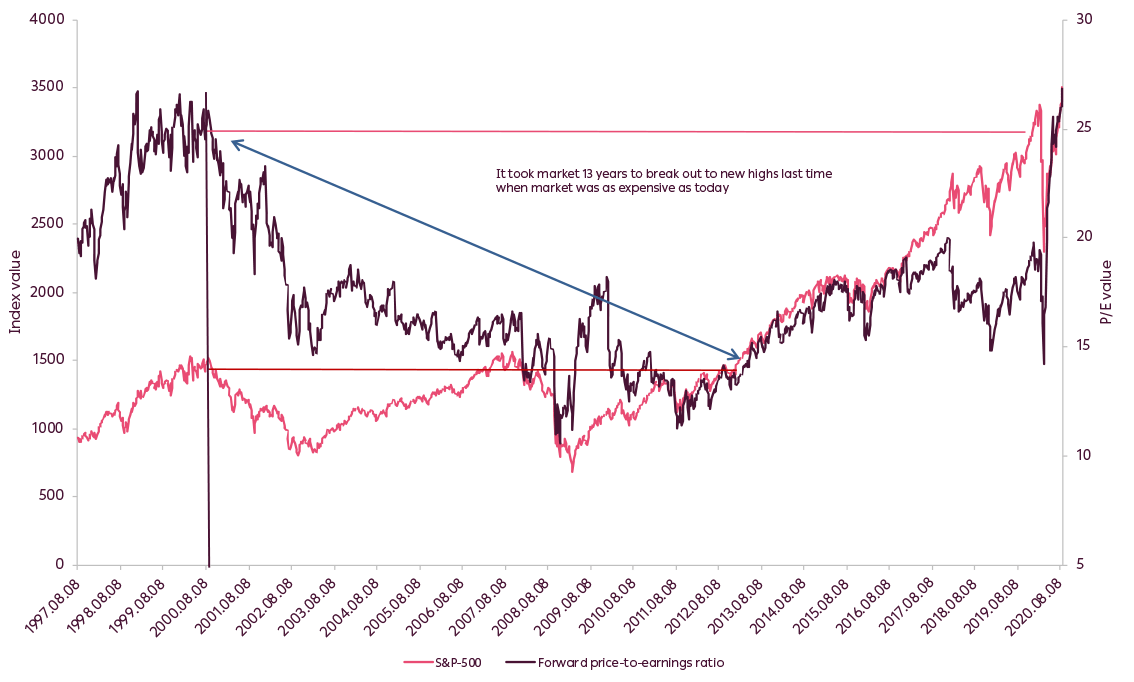

Considering the extremely low interest rate environment, stocks still manage to provide a decent risk premium over bonds, as earnings are expected to gradually rebound, while many bonds are yielding close to 0. However, stock market valuations are at highest level since late 90s while economy is undergoing one of the most severe economic recessions in recent history, so chasing the market currently may turn out quite risky. Remember, when equity indices toped in 2000, US indices were not able to surpass that highs for 13 years after that, while majority of European indices have not surpassed 2000 ever since. That is why despite what might be one of the strongest equity rallies in USA, it makes sense to stay calm and not follow speculative impulses to aggressively pursue such rally but to pursue long term investment goals instead.

S&P-500 performance and valuation

Source: Bloomberg

1Acronym for Facebook, Apple, Netflix, Microsoft, Amazon, Alphabet (Google)

2These companies are Tesla and Apple

3Market sell-off in early September provides partial evidence of this risk

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.