The winter of European discontent has passed | Luminor

The winter of European discontent has passed

- European Central Bank has raised the rates – again

- Energy crisis in Europe recedes, economy resilient

- Strong numbers from the US jobs market, although times ahead could be rough

After starting the year at an especially optimistic tone in January, financial markets have retreated a bit during February, digesting the conflicting views on the resilient economy, slowing inflation and still predominantly hawkish central bank stance around the world. The developed countries‘ stock market index MSCI World has decreased slightly by 2.5 %, whereas the emerging markets stocks‘ gauge MSCI Emerging Markets has feared worse by hitting the negative 6.5 % returns levels in February.

ECB hikes again

In the beginning of February, the European Central Bank (ECB) decided to raise the key rate by 0.50 % to 2.5 %, thus extending the extraordinary set of interest rate increases started last year. Despite the record pace of the hike cycle so far, the Governing Council of the ECB said in a statement that it „intends“ to raise the rates by yet another 0,50 % in its next meeting in March before evaluating next steps in the monetary policy. Christine Lagarde, the President of the ECB, has reiterated the usual strict position on the further hikes by assuring the market that “our determination to reach 2 % medium‑term inflation

should not be doubted”.

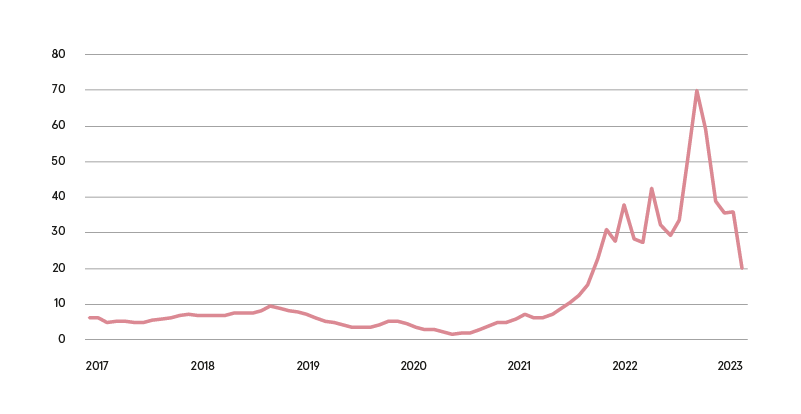

Energy crisis in Europe recedes

Energy prices in Europe definitely contribute to the ECB ambition of slower inflation, as they have been receding in the recent past. Perhaps most strikingly, natural gas prices in Europe have continued trending down to reach the lowest levels since late 2021 and dropping more than three times since the 2022 August peak. While the risk of price spikes remains, the unusually warm winter season, the unprecedented pace in implementing new liquid natural gas (LNG) import capacity and restrained natural gas demand have all certainly contributed to calming the energy markets.

Natural gas prices in Europe, USD/MMBtu

Source: Bloomberg L.P.

Signs of European recovery

As if to underline the recovering mood in the European economy, S&P Global’s Eurozone Composite purchasing managers’ index (PMI), which measures the level of activity in manufacturing and services, increased to 52.3 in February (from 50.3 in January) and exceeded the forecasted level of 50.6. The reading essentially tells that the business activity in the bloc has been expanding (readings above 50) for the second month in a row, thanks to resilient services’ activity and recovering manufacturing activity.

US economy in crossroads

In the meantime, the US economy has been showing conflicting signs over the recent month. Market participants have been surprised by the US economy adding extremely strong 517,000 number of jobs in January versus 187,000 expected (and versus the previous reading of 260,000). The news have sure contributed to the renewed hopes of “soft‑landing” in the economy – mild slow down, only, in the economic activity amid slowing inflation. On the other hand, investors’ optimism was daunted by the retail behemoths’ – Walmart (supermarkets) and Home Depot (home improvement retail) – shared concerns of tougher times ahead as consumers are expected be more frugal in 2023.

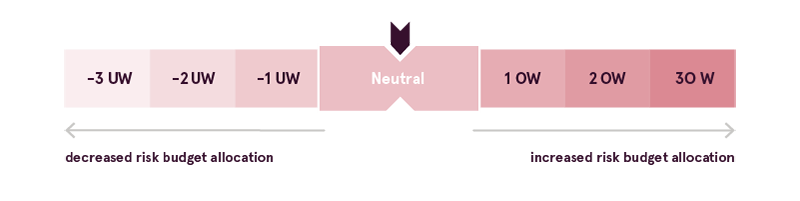

“House view” update

Thanks to the conflicting views in the world economy, we decided to retain the neutral risk allocation budget. As the indicators show improving market sentiment and economic activity, we have been reducing our positioning towards the defensive industries, while not entering the more growth‑oriented industries’ positioning, for now.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.