Important: Predicted amount of money to be accumulated in a pension fund is not guaranteed. The examples of calculations given are for information only and should not be understood as investment recommendation. Saving in pension funds incurs investing risk, which means that investments may rise or drop in value, return may be smaller than investment. If investment in a foreign currency is made into financial instruments, exchange rate changes may affect the return of investment. Luminor Investment Management does not guarantee the return of investment, profitability of pension funds or amounts of annuities to be paid. Past results of pension funds do not guarantee future results. Before deciding on complementary retirement savings in Luminor savings funds, read the rules of the pension funds, deductions applied, investment strategy and risk factors. Pension funds are managed by Luminor investicijų valdymas UAB, company code 226299280.

30-44

If you already saving in the 2nd and 3rd pension pillar funds – you are on the right track. Your money is continuously invested. The longer you save, the more money you can expect to accumulate to grow old with dignity.

However, do not forget to check if you ensure maximum saving in the 2nd pension pillar fund (at the same time, receive maximum state incentive) and is your 3rd pension pillar saving strategy is adequate – book a consultation here.

You have not started saving yet? Start saving and improve your financial situation when retired.

Making regular monthly contributions of EUR 50 into your 3rd pension pillar fund presuming the average yearly return of 4.5%*, in 30 years you can expect to have extra EUR 34 500 on your pension account. 3rd pension pillar is attractive for its flexibility - you decide how much, how often, in how many funds to save, how and when to receive benefits.

Knowing that time is running fast - we suggest you to consider a possibility to start saving for retirement as soon as possible. The earlier you start - the more you are likely to save:

Your accumulated amount at the age of 65 if you started accumulating at the age of 32, 38 or 44, EUR*

| Monthly contribution | 32 y. o. | 38 y. o. | 44 y. o. |

|---|---|---|---|

| EUR 30 | 24 816 | 17 192 | 11 338 |

| EUR 40 | 33 088 | 22 923 | 15 117 |

| EUR 50 | 41 360 | 28 653 | 18 896 |

| EUR 100 | 82 720 | 57 307 | 37 792 |

* Based on the calculations and presumptions of Luminor pension calculator. Balanced (average yearly return of 4.5%) investing strategy and compound interest principle applied, i.e. when money is earned not only from the initial invested amount but also from accrued interest, were used in the calculations. For more information: luminor.lt/pensiju-skaiciuokle.

The presented results do not include deductions applied by pension funds. Pension fund documents containing comprehensive descriptions of the properties of this product, including characteristic risks and applied deductions are available here.

You have no idea what pension pillars are and if you are their user? We have a short FAQ for you:

What are the differences between 1st, 2nd and 3rd pension pillars?

Lithuanian pension system consists of three pillars:

- 1st pillar – state social security pension. 1st pension pillar is a mandatory part of the saving system and if paying social security contributions, you participate in it. Contributions are converted into points, depending on your salary, while in the future your pension will be determined by the number of points. The amount of a pension paid by SODRA depends also on the ratio between workers and pensioners and economic situation.

- 2nd pension pillar – a type of saving for retirement, when money contributions are directly related to the amount of a pension. When saving in the 2nd pension pillar fund, monthly contributions are transferred automatically. A certain share of your salary, plus the state incentive, are transferred to the pension fund. Differently from the 1st pension pillar, money deposited in the pension fund is your property and heritable. Are you participating in the 2nd pension pillar fund? If you work and have not chosen otherwise, most probably you are participating. Find out more

- 3rd pension pillar works the same way as the 2nd pillar, however it is a volunteer saving mode: you can decide on the contribution amount and frequency of contributions. The Government promotes saving by applying 20% tax privilege on paid contributions, which can amount up to EUR 300 per year. Find out more

How do pension funds work?

Pension fund managers invest participants' contributions held in 2nd pension pillar fund in accordance with the investing strategy. It means that every saved Euro for retirement is invested to earn extra return.

Funds are divided by their investment strategies: In pursuit of optimum return on investment, we suggest choosing the fund according to your age: for younger people, we recommend a fund investing into shares, and closer to the retirement age – into fund with majority of bonds in its assets, and smaller part of shares to reduce short‑term fluctuations of accumulated asset value.

From 2019, the 2nd pension pillar funds are managed following the life cycle approach. Saving in a pension fund is convenient as it is adapted to your date of birth and selected automatically. The younger you are, the bigger investments into share markets are made in pursuit of bigger return on investment. With the retirement age approaching, the proportion of shares in the fund (and risk) is gradually decreased, while the share of bonds and other safer investment instruments (deposits, money) is increased to protect the saved funds. You are free to choose an investment strategy of your 3rd pension pillar fund, however we suggest following the same life cycle approach: youngers should choose a fund investing into shares, and with the retirement age approaching – a fund with bigger investment into bonds and smaller into shares.

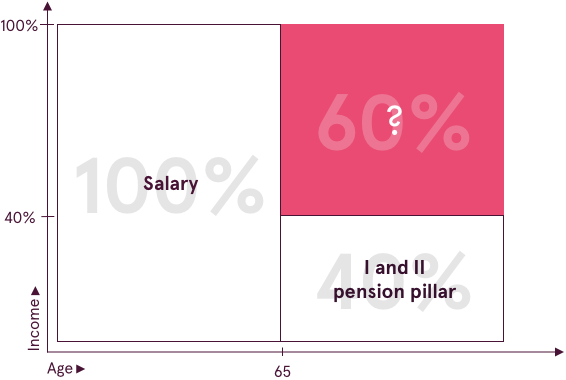

How much should I save for old age?

To understand what incomes you can expect when retired, you should analyse your present situation. Consider your salary, savings, investments made by now or other assets. All this could help you to assess your financial situation today and to answer the question, how much extra savings you need. According to financial experts, for financially secure old age, you need 70‑80% of your current monthly incomes. With the help of the pension calculator, find out your future pension. Calculate

What if I am self-employed?

If you do not work by employment contract, you should check what potential 1st pension pillar is forecasted for you and if you can join the 2nd pillar. It is very likely that for financially secure old age, you will have to rely more on the 3rd pension pillar funds or other personal savings. More

Register for consultation about pensions